Value Added Tax (VAT) is a key element of the Bulgarian tax system, which we discussed in the previous article. It affects both businesses and consumers. However, there are certain circumstances under which VAT is not charged. Understanding these scenarios is essential for the effective management of your business and compliance with tax legislation.

When is VAT not charged?

There are several main situations in which VAT is not charged:

- Lack of VAT registration: If your business is not registered under the Value Added Tax Act (VATA), you are not obligated to charge VAT on the goods or services you provide.

- Special registration regimes: Even in cases of certain types of VAT registration, such as registration under Article 97a (for receiving services from foreign entities) or Article 99 (for intra-community acquisitions), you may not be required to charge VAT on your supplies.

- Exempt supplies: Some supplies are legally exempt from VAT. These include services related to healthcare, social care, education, culture, financial and insurance services, as well as transactions involving certain real estate properties.

- Supplies with a place of supply outside Bulgaria: When the place of supply is outside the territory of the country, VAT is not charged. This is commonly the case with exports of goods or the provision of services to clients outside Bulgaria. However, it is important to assess each case individually.

Lack of VAT registration

In Bulgaria, VAT registration is mandatory upon reaching a certain turnover threshold. If your annual turnover is below the established threshold of 166,000 BGN, you are not required to register for VAT and, accordingly, do not charge VAT to your clients. This can be an advantage for small and start-up businesses, as it simplifies accounting and reduces the administrative burden.

How is the turnover for mandatory registration calculated?

The turnover for VAT registration is calculated based on taxable revenue over the last 12 consecutive months, rather than just the current calendar year. This means that even if your turnover does not reach 166,000 BGN in a given year, but this threshold is exceeded within the previous 12 months, registration becomes mandatory.

For example:

- If the turnover in January is 10,000 BGN and in February is 12,000 BGN, but revenue increases sharply in the following months and by December reaches a total of 170,000 BGN for the last 12 months, VAT registration becomes mandatory, even if turnover was lower until October.

- If the threshold of 166,000 BGN is reached in March, the company or individual has 7 days to submit a registration application to the National Revenue Agency (NRA).

Special Registration Regimes

Even with VAT registration, there are special regimes under which VAT is not charged on certain supplies.

Registration under Article 97a of the VATA

This regime applies to entities that are not registered for VAT but receive services from foreign suppliers where the place of supply is in Bulgaria. Most commonly, this concerns businesses purchasing online advertising services, software licenses, hosting, or consultancy services from companies based outside the country.

A key point here is that although the entity is not VAT-registered due to its turnover, it is still required to register under Article 97a and self-charge VAT on the received service. In this case, the company is not entitled to a VAT credit, but it is obligated to declare and pay the corresponding tax.

Registration under Article 99 of the VATA

This regime applies to entities that are not VAT-registered but engage in intra-community acquisitions of goods, i.e., they purchase goods from other EU countries. In this case, if the total value of intra-community acquisitions exceeds 20,000 BGN in a calendar year, registration under Article 99 becomes mandatory.

Under this regime, the entity does not charge VAT to its customers but must self-charge VAT on the acquired goods and report it to the National Revenue Agency (NRA). This registration does not allow VAT credit deduction, but it is compulsory if the threshold of 20,000 BGN is exceeded.

Example:

A Bulgarian business that is not VAT-registered purchases equipment worth 25,000 BGN from Germany. Since the amount exceeds 20,000 BGN, the business is required to register under Article 99, self-charge VAT, and report it to the NRA.

Exempt Supplies

The law provides a list of supplies that are exempt from VAT, but the exemption is not automatic—to apply it correctly, entities performing such supplies must meet specific legislative requirements and possess the necessary documentation.

What are the criteria for VAT exemption?

For a supply to be VAT-exempt, it must fall within the specific categories described in the Value Added Tax Act (VATA). At the same time, the supplier must have proof of the nature of the goods or services provided.

For example:

- Medical Services: VAT exemption applies only to licensed healthcare facilities and medical professionals providing services related to diagnosis, treatment, and prevention. If a healthcare facility offers additional services, such as aesthetic procedures that are not directly related to healthcare, these services may be subject to VAT.

- Education: Only accredited educational institutions and certified training organizations can benefit from VAT exemption. Courses conducted by private training centers or individual instructors without accreditation may be subject to VAT.

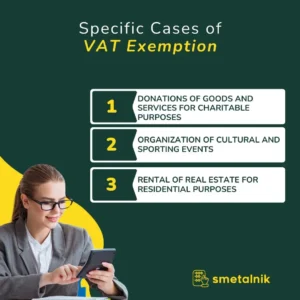

Specific Cases of VAT Exemption

In addition to the main categories, there are also some more specific types of supplies that may be exempt from VAT under certain conditions:

- Donations of goods and services for charitable purposes – if they meet legal requirements and are directed towards non-profit organizations registered for public benefit activities.

- Organization of cultural and sports events – if the events are held by recognized institutions or non-profit organizations.

- Rental of real estate for residential purposes – under certain conditions, if the property is not used for business activities.

Documentation and Accounting Compliance

To benefit from VAT exemption, businesses and individuals providing such supplies must maintain strict accounting records and possess proof of the grounds for exemption. This may include:

- Licenses and registration documents for the relevant activity (e.g., a license for a medical facility or accreditation certificate for an educational institution).

- Contracts, invoices, and financial records proving the nature of the supplied goods or services.

- Declarations for VAT-exempt supplies, which may be required during tax audits.

Supplies with a Place of Supply Outside Bulgaria

When goods or services are supplied with a place of supply outside Bulgaria, VAT is not charged. This is because VAT taxation occurs in the country where the recipient is registered, according to the principles of international trade taxation.

Specific Cases of Different Types of Supplies

Export of Goods to Third Countries (Non-EU States)

- Supplies of goods outside the EU are subject to a 0% VAT rate.

- To apply the zero rate, the exporter must have customs documents (EAD – Export Administrative Declaration) proving that the goods have left the EU territory.

- If the necessary documents are missing, VAT may have to be charged, even if the goods have physically left the country.

Intra-Community Supplies (Sales Within the EU)

- If the supply is made to a VAT-registered company in another EU member state, VAT is not charged, and the recipient is obligated to declare the transaction under the reverse charge mechanism.

- The supplier must verify the validity of the customer’s VAT number in the VIES (VAT Information Exchange System) to ensure that the transaction qualifies for VAT exemption.

Services Provided to Foreign Clients

- When services are provided to clients established outside Bulgaria, the place of supply determines whether VAT should be charged.

- For services such as consulting, digital marketing, software development, design, and other intangible services, the place of supply is typically the recipient’s country, meaning that VAT is not charged in Bulgaria.

- If the client is a VAT-registered company in the EU, the reverse charge mechanism applies. If the client is outside the EU, the service is not subject to VAT in Bulgaria.

Documentary Justification

To apply VAT non-chargeability for supplies with a place of supply outside Bulgaria, businesses must have evidence proving that the transaction falls under this category. Depending on the type of transaction, this may include:

- Customs documents (for exports).

- Transport documents (CMR, waybills).

- Contracts with foreign clients specifying the place of supply.

- VAT registration confirmation of the recipient in the EU (for intra-community supplies).

- Payment orders proving receipt of funds from abroad.

Conclusion

A proper understanding of VAT non-chargeability is crucial for any business aiming to comply with legal requirements and optimize its tax obligations. Depending on the specifics of the activity, legislation provides various scenarios where VAT is not charged, but applying these rules requires precision and thorough knowledge of tax regulations.

To avoid mistakes and ensure compliance with current laws, seeking professional accounting consultation is highly recommended. This can help in better tax planning and efficient financial management.

For more interesting and useful articles, visit the Smetalnik blog!