When we hear about royalties and licensing fees, we always think of freelancers in the creative industries. These fees can be mixed, including both payments for labour and compensation for the right to use the copyrighted work.

For freelancers, it is extremely important to understand what taxes and social security contributions apply to these earnings.

Mixed Copyright Agreement: What Is It?

A mixed copyright agreement is a contract in which payment is made for the creation of a work and the right to use that work.

An example of such a contract is when a designer creates a logo for a client and, at the same time, transfers the rights to use it. The portion of the payment for designing the logo is taxed as labour income, while the portion for the rights to the logo is taxed as a licensing fee.

Taxes on Copyright Earnings: Labor and Licensing

The tax treatment of copyright earnings is a key aspect of financial planning for any artist or freelancer who creates and distributes works.

The distinction between labour income and licensing fees is crucial for determining the applicable taxes.

Licensing Fees: Tax Rate and Application

Licensing fees represent income earned from granting rights to use a copyrighted work. This includes licensing agreements where the author transfers the right to use their work for a specific period or under certain conditions. Examples include software, books, music, films, or other creative content contracts.

Licensing fees are treated differently from labour income, not so much in tax rates but in allowable expense deductions that can be applied to the income. In Bulgaria, licensing fees benefit from higher recognized expense deductions, effectively reducing the income’s taxable portion.

Examples of Licensing Agreements

- Music Rights – A composer who grants rights for their music to be used in films or commercials receives a licensing fee. This fee is subject to a 10% tax, making it more favourable than direct payment for creating the music.

- Software Licenses—Software developers may license their programs to various companies. Instead of being paid for project work, the developer receives licensing fees, which are taxed at a lower rate.

Distinction in Mixed Payments

In mixed payments, where part of the income is for labour and another part is for granting rights, it is essential to determine the correct ratio between these two components.

Incorrectly allocating this ratio can result in higher tax liabilities and potential penalties from tax authorities.

Example: If a writer signs a contract with a publisher where 70% of the payment is for writing the book and 30% for its rights, they will pay different taxes on each portion. However, if the contract does not clearly define this ratio, tax authorities may interpret the entire payment as labour income, leading to significantly higher tax and social security obligations.

International Licensing Agreements

One of the challenges faced by authors working internationally is the different tax treatments in other countries.

For example, if a Bulgarian author sells licensing rights to a foreign client, taxes may be levied in Bulgaria and the buyer’s country. In such cases, double taxation avoidance agreements typically apply, which can significantly reduce the author’s financial burden. However, it is crucial to comply with these agreements and submit the declarations carefully.

Social Security Contributions on Payments for Creation, Use, and Transfer of Works

To properly manage social security contributions, authors must understand how different types of payments—whether for labour, usage, or transfer of works—are treated under the law.

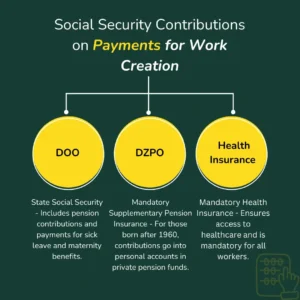

Social Security Contributions on Payments for Work Creation

When an author is paid for creating a work (such as writing a book, creating graphic artwork, or composing music), this income is treated as labour income. It is subject to health and social security contributions, including pension and other social security risks.

Mandatory social security contributions are distributed as follows:

- State Social Security (DОО) – Includes pension contributions and payments for sick leave and maternity benefits.

- Health Insurance – Ensures access to healthcare and is mandatory for all workers.

- Mandatory Supplementary Pension Insurance (DZPО) – For those born after 1960, contributions go into personal accounts in private pension funds.

Depending on the specific activity, the author must contribute based on the minimum insurable threshold set for freelancers. Contribution amounts vary depending on whether the individual is registered as self-employed (freelancer) or operates through a company. Social security contributions are mandatory regardless of whether the author has other income sources (such as rental income or dividends).

Social Security Contributions on Licensing Fees

Unlike labour income, licensing fees—those received for granting usage rights to work—are not subject to social security contributions. This is a significant relief for authors who primarily earn through licensing their works, as they are not required to pay social security contributions on this type of income.

For example, if a photographer sells the rights to use their photo for advertising purposes, they will not owe social security contributions on that payment. The only obligation the author will have is to pay a 10% tax on the licensing revenue.

Social Security Contributions on Work Transfers

The transfer of copyright (such as selling the permanent right to use a work) is also not subject to social security contributions.

This means that when an author entirely sells the rights to their work, such as in the case of book publishing or software sales, they will owe only taxes but will not be required to pay social security contributions on the received income.

This makes the transfer of copyright an attractive option for creators looking to reduce their social security obligations. However, to ensure proper tax and legal treatment, the contract should clearly specify the nature of the payment—whether it is for labor, usage, or transfer of rights.

Important for Proper Social Security Planning

Authors must carefully plan their contracts and earnings to avoid unnecessarily high social security contributions.

One of the challenges they face is correctly dividing their income into labour and licensing portions to benefit from the lower social security obligations on licensing fees. If the entire payment is classified as labour income, social security obligations can significantly increase the total tax burden.

Tax Relief Opportunities

Tax legislation provides several mechanisms to reduce the tax burden on income earned from copyright fees. These reliefs can be useful for freelancers and those creating works as part of larger projects or organizations.

Deducting a Percentage of Income as Recognized Expenses

Bulgarian tax law allows authors to deduct a certain percentage of their income as recognized expenses. For authors, this percentage is typically 40% of total revenue. This means that 40% of the income is not subject to taxation, significantly reducing the tax burden.

Example: If an author receives BGN 10,000 in royalties for a creative work, 40% (or BGN 4,000) can be deducted as recognized expenses. The remaining BGN 6,000 will be subject to a 10% income tax.

Tax Relief for Reinvestment

Authors who reinvest their income in new projects or materials to create works can use this opportunity to reduce their tax burden.

Reinvesting in new projects, equipment, training, or software is recognized as an expense, meaning the invested amounts can be deducted from taxable income. This method helps authors lower their tax liabilities and improves their skills and resources for future projects.

Tax Relief for Foreign Income

Authors who receive royalties from foreign sources can benefit from double taxation avoidance agreements that Bulgaria has with multiple countries. These agreements allow authors to avoid being taxed twice—once in Bulgaria and once in a foreign country. To take advantage of this opportunity, authors must provide the necessary documents proving that they have already paid taxes abroad.

Specialized Tax Reliefs for Cultural and Creative Industries

Some creators may benefit from specific tax reliefs for cultural and creative industries.

For example, the government sometimes provides subsidies or reduced tax rates for projects that have cultural significance. This includes support for films, music projects, literature, and other art forms. Creators in these categories should check the available tax relief programs, which can provide significant financial assistance.

Tax Relief for Donations

Authors who make donations to cultural projects, charitable organizations, or other recognized causes can also receive tax relief. In Bulgaria, up to 5% of taxable income can be deducted for donations to public-benefit initiatives. This encourages both support for social causes and the reduction of tax liabilities.

Example Table of Tax Reliefs:

Avoiding Tax Risks and Penalties

Authors must use tax reliefs lawfully. Incorrect expense deductions, lack of transaction documentation, or incorrect income declarations can lead to tax audits and severe penalties.

This is why it is recommended for creators to work with an accountant or tax consultant to ensure they apply reliefs correctly and avoid tax risks.

In conclusion, authors have multiple opportunities to reduce their tax burden when earning royalties and licensing fees, provided they properly plan their income and take advantage of the legal reliefs available. This will optimize their financial situation and allow them to focus on creating new creative works.

If you want to learn more about the accounting aspects of creative professions, check out our blog, where we share useful tips and insights. We especially recommend reading our article on tax and social security requirements for artists, which provides an in-depth look at specific cases in this field.