How self-insured persons can receive sick pay: insurance length, documents, and deadlines from the NSSI

The professional path of a self-insured person – be it a craftsman, a freelancer, or a partner in a commercial company – is marked by independence, but also by the need for self-management of all aspects of their activity, including social security. When illness occurs or there is a need to care for a family member, the question of receiving cash compensation for temporary incapacity for work, popularly known as “sick pay” or “sick leave,” arises. This process is governed by the Social Security Code (SSC) and requires excellent knowledge of the specific conditions and strict adherence to procedures.

Unlike employed persons, where the employer is the main driver of the process, the self-insured person bears full responsibility for their correct insurance coverage and the timely submission of documents to the National Social Security Institute (NSSI).

Key Condition: Insurance for “General Sickness and Maternity”

The first and most essential point is related to the choice of insured risk. The law obliges self-insured persons to be insured for disability due to general illness, old age, and death. The right to compensation for temporary incapacity for work (the so-called sick pay) is acquired only if the person has explicitly chosen to contribute for the risk “General Sickness and Maternity” (GSM).

This choice is declared to the National Revenue Agency (NRA) upon commencing activity or when changing insurance coverage. If this additional risk is not chosen, the person is not entitled to cash compensation from the NSSI in case of illness, regardless of the issuance of a sick leave certificate.

Minimum Insurance Length Requirements

Once the choice to insure for GSM is made, the person must accumulate a minimum insurance length for this risk. To acquire the right to cash compensation due to general illness or for caring for a sick family member, the self-insured person must have at least six months of insurance length as an insured person for “General Sickness and Maternity.” This length may include insurance acquired on another basis, provided that insurance for the same risk was also paid there. If the required length is not accumulated, the NSSI will not pay compensation.

The Amount of Compensation is Linked to the Insurable Income

The cash compensation is calculated at 80 per cent of the average daily cash compensation. This average daily compensation is determined based on the insurable income on which contributions were paid, for a period of eighteen calendar months preceding the month in which the temporary incapacity for work occurred.

The insurable income that the self-insured person declares and contributes on must be within the limits set by the State Social Insurance Budget Law (SSIBL). For 2025, the minimum monthly insurable income for self-insured persons is set at 1077 Leva. To ensure a higher amount of compensation in case of illness, the person must have declared and paid contributions on a larger insurable income, in compliance with the maximum monthly insurable income for the country.

Important Note: Unlike employed persons, for self-insured persons, the NSSI pays the compensation from the first day of the temporary incapacity for work, provided all requirements are met.

Procedure for Submitting Documents to the NSSI

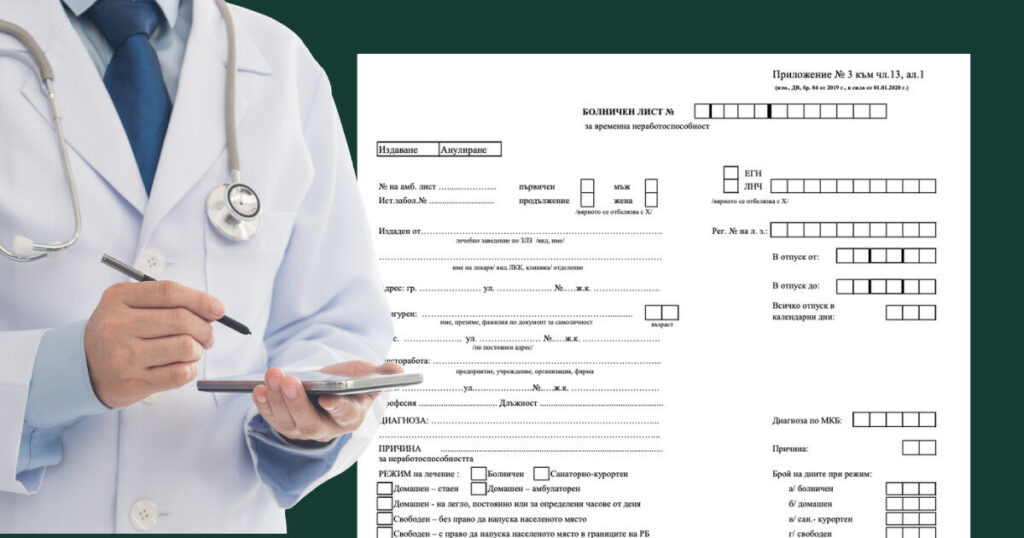

After the electronic sick leave certificate is issued by the attending physician, it is sent officially to the NSSI. Despite this, the self-insured person has the obligation to submit a Certificate regarding the right to cash compensation to the NSSI, which is known as Appendix No. 11 to the Regulations for Calculating and Paying Cash Compensations and Aids from the State Social Insurance (DSI).

- Submission Deadline: The document must be submitted by the 10th day of the month following the month of the sick leave certificate’s issuance.

- Method of Submission: Submission is done electronically through the NSSI portal, mandatorily using a Qualified Electronic Signature (QES). This can be done either personally by the person or by an authorized representative.

The accurate and timely submission of Appendix No. 11 is critical for the quick receipt of compensation. Any error or inaccuracy in the filled-in data, as well as a missed deadline, can lead to a delay or refusal by the NSSI.

Recommendation: The Role of Licensed Accounting Services

The complexity of the social security legislation, the specific requirements for declaring insurable income, the mandatory submission of Declarations Form 1 and Form 6 to the NRA, and the strict procedure for submitting Appendix No. 11 to the NSSI, make the use of licensed accounting services highly recommended.

A professional accountant ensures not only correct current accounting but also peace of mind for the self-insured person by:

- Guaranteeing the correct choice of insurance for GSM and compliance with the minimum and maximum insurable income.

- Monitoring compliance with all deadlines for the NRA and NSSI.

- Preparing and submitting Appendix No. 11 with QES, eliminating the risk of errors in the documentation that would delay the payment of funds.

Experience shows that investment in accounting services is an investment in security and the continuity of the financial flow, especially when the person is prevented from working due to a health problem. Trusting experts allows the self-insured person to focus on their recovery instead of struggling with administrative challenges.

In summary, the right to cash compensation for temporary incapacity for work for self-insured persons is clearly regulated, but it requires proactivity, an informed choice, and strict adherence to the legal provisions. Correct insurance for “General Sickness and Maternity” and working with a competent accountant are the main pillars that guarantee financial stability in case of illness.