The patent tax is a specific form of taxation applied to certain activities and professions in Bulgaria. This tax is aimed at small and medium-sized entrepreneurs engaged in specific activities listed in the law.

In this article, we provide comprehensive information about the patent tax, including how to calculate it, who is required to pay it, its amount, and the procedures for payment. It will be particularly useful for freelancers and self-employed professionals who need clarity on this subject.

What is the Patent Tax, and Which Activities Does It Cover?

The patent tax is a fixed annual tax applied to certain activities listed in the Local Taxes and Fees Act (ZMDT). It is primarily targeted at small businesses and individuals engaged in patent-based activities whose annual revenue does not exceed 166,000 BGN.

The main characteristic of the patent tax is that it is not calculated based on the taxpayer’s actual income but rather on the type and location of the activity. This makes it particularly suitable for professions and businesses with unpredictable or highly fluctuating revenues.

The difference between the patent tax and personal income tax lies in the calculation method—the patent tax does not depend on actual earnings but is instead determined by administrative criteria related to the type of business and location.

The legislative framework regulating the patent tax includes the Local Taxes and Fees Act (ZMDT) and relevant municipal regulations. These determine the specific rates and payment conditions, which vary across different municipalities.

Who Is Required to Pay the Patent Tax?

The patent tax applies to **individuals, sole traders, and legal entities** engaged in certain activities.

List of Activities Subject to the Patent Tax

- Retail trade (including small shops and kiosks with a commercial area of up to 100 sq.m.).

- Food establishments (cafés, restaurants, and bistros, excluding fast-food establishments).

- Hairdressing and beauty services (beauty salons, hairdressing services, manicures and pedicures).

- Craft services (locksmiths, shoemakers, tailors, watchmakers, and similar services).

- Repair services (repair of household appliances, TVs, and computers).

- Automotive services (car washes, auto repair shops, bicycle repair services).

- Tailoring and leatherworking services.

- Photography services (photo studios and photography services).

- Hotels and guesthouses (small accommodation facilities with up to 20 rooms).

- Transportation services (taxi passenger transport).

- Private kindergartens and daycare centres, private educational centres, and schools (non-accredited educational and training services).

A business or individual must meet specific conditions to be subject to the patent tax, one of which is having an annual turnover that does not exceed 166,000 BGN.

Additionally, not all activities qualify for the patent tax— freelance professions such as lawyers, accountants, and doctors are not covered under this regime. Moreover, businesses operating in multiple municipalities or those registered under the Value Added Tax Act (VAT Act) are not subject to the patent tax.

Patent Tax Rates

The amount of the patent tax in Bulgaria varies depending on several key factors, including the **location of the business**, the **type of service or trade**, and the **specific nature of the activity**. In larger cities such as Sofia, Plovdiv, and Varna, tax rates are significantly higher than in smaller towns due to the greater economic potential and higher revenue-generating capacity.

Moreover, **the type of activity** also plays a key role in determining the tax amount. Different professions and business categories are classified into groups, each subject to different tax rates. For example, a small retail shop and taxi services may have different tax rates even if they operate in the same city. The tax amount is calculated based on criteria such as shop size, number of employees, or service capacity.

The exact tax rate is determined by the respective municipality and published in municipal regulations on local taxes and fees. Every business should review the applicable municipal regulations to understand the requirements and specific rates.

Examples of Tax Rate Differences

- Retail trade in Sofia, in a shop with an area of up to 100 sq.m., may be subject to a patent tax of 600–1,000 BGN per year, depending on the specific location within the city.

- Hairdressing and beauty services in smaller towns like Lovech or Sandanski may have significantly lower tax rates—200 to 400 BGN per year.

Patent Tax Payment Procedure

The payment process begins with submitting a patent tax declaration to the local municipality where the business operates. The declaration must be submitted at the beginning of the year or upon starting a new business.

Steps for Filing the Declaration:

- Filling out the patent tax declaration

The form can be obtained from the municipality or downloaded from its website. It should include all necessary details, such as business type, new or existing registration, and key parameters affecting tax calculation. - Submitting the declaration

The declaration can be submitted in person at the municipality or electronically through the municipality’s website (if available). Online submission is preferred as it saves time and minimizes errors.

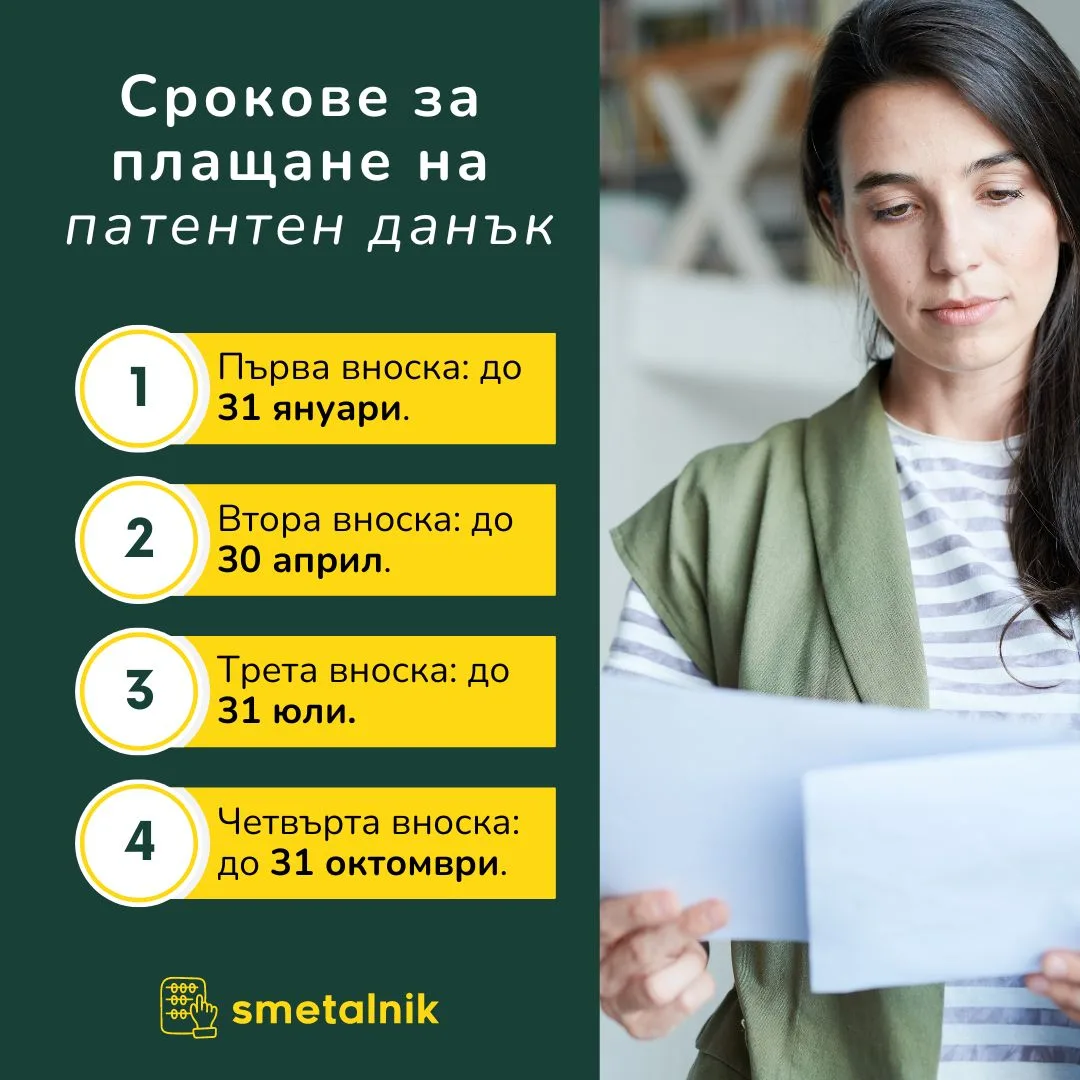

Patent Tax Payment Deadlines

Payments are made in quarterly instalments, with specific dates announced by the municipality each year. Late payments or incorrect tax calculations may result in penalties and interest charges.

To avoid issues, it is recommended that you consult a professional accountant or specialist for assistance in preparing and submitting the tax declaration.

Summary of Patent Tax Advantages and Disadvantages

Conclusion

The patent tax offers advantages and drawbacks for self-employed professionals. Consulting a tax specialist is highly recommended to ensure compliance. For additional insights, visit the Smetalnik blog for more informative content.